How FinServ Helps Funds Optimize Their Operations

Operational assessments provide an opportunity for asset managers to objectively evaluate current operational structures with an eye toward improving operations. Today’s environment — characterized by hybrid work structures and new strategies focused on investments in cryptocurrencies and other alternative assets – means that managers need to initiate these assessments to ensure that existing systems and processes are aligned with long-term operational goals.

There are many reasons for an asset management company to undertake an operational assessment. The most common are that firms grow assets under management, change or add the types of assets traded, expand the range of strategies and/or funds it manages and have a more complex investor base with different requirements for shareholders. All these changes mean systems and processes set up at the beginning of the firm’s life cycle may no longer be fit for purpose.

FinServ Consulting leverages all its experience and expertise gained in working with similar funds or businesses to help support its clients in this exercise. This has given the company unique insights into how assessments can be conducted and what asset management firms will gain from the process.

Identifying Problem Areas

The first step in the process is to look at and analyze an investment firm’s full operations and processes to identify inefficiencies that are holding back the growth of the firm. This process can also reassure investors that the firm is doing everything it can to use its resources effectively while at the same time having processes and controls in place to ensure that operations from front to back office are running smoothly and are fit for the present as well as the future.

The assessments can highlight a variety of areas where firms may want to make changes. This strategic initiative looks at how technology is being used, whether service providers deliver in the most effective way and if teams are structured for optimal efficiency. The review can expose bottlenecks, suggest areas where best practice can be implemented and show how to streamline a business. Ultimately, a target operating model is defined and presented with a path to get there.

Although operational assessments are routinely conducted by many firms, lately there has been an increase in requests for these evaluations. This is due to several reasons. For example, because of the pandemic, some technology investment has been delayed however, firms have only grown in complexity. Inefficiencies caused by manual processes may be exacerbated as the fund grows its assets under management (AUM).

Many firms still use Excel or have many operations done manually when there are more eloquent automated solutions available. The frequency of this can be a direct result of the infrastructure set up at the beginning of a firm’s life cycle. As it grows, those processes may no longer be adequate, particularly if it has experienced changes in the types of asset classes traded, the size and volume of trades or other factors. These factors mean existing infrastructure is less optimal. The systems used at the start of a business may not be scalable or the most efficient as it grows.

Identifying Where Efficiencies Can Be Made

Once the parameters of the operational assessment are established, everyone involved in a specific process in a fund are interviewed using a set list of questions. This helps identify ways to streamline work – such as trading workflows.

For instance, portfolio managers do not always have all the information they need at their fingertips. There may be a lot of manual work before a trading decision is made. Interviews with portfolio managers, traders, operations, finance, and anyone from the technology side involved in these processes are interviewed to identify areas where there may be ways to update work streams or plan for future expansion.

A list of predetermined questions also gives the conversations a focus and helps identify areas of inefficiency that can be improved.

The resulting list of projects – ways a firm can change processes, technology and even people to be more efficient – can be daunting. These projects can be small or large, complex or simple, easy to implement or difficult.

While it is always up to the firm to decide which projects it wants to tackle in the short or long term, some like to focus on quick wins that may be relatively inexpensive while others put together a program aimed at gradual transformation of processes and procedures.

FinServ Consulting has developed a project impact/effort matrix that helps identify which actions will have the most impact on the business while also judging the difficulty or complexity in implementing these compared with those that are much easier to do but have less overall effect on the business.

This assessment is a snapshot, giving the firm an overview of inefficiencies and what the impact of fixing them will be. Quick wins could include things like reorganization of the folder directory, discontinuing daily reports or giving Bloomberg access to more people. Key improvements that may take longer to implement might include hiring more people, like a tax director, implementing new systems like a portfolio management system (PMS) or a data warehouse.

The addition of new strategies and funds may also put a strain on existing infrastructure. Likewise, the introduction of managed accounts, funds of one or onshore/offshore structures to accommodate a wider range of investors will necessitate different procedures and processes.

Operational due diligence by investors can also identify red flag areas where improvements need to be made.

A Path Forward: Recommendations

At the end of the operational assessment there are usually five to six strategic areas where change is recommended. These range from relatively inexpensive projects to more long-term changes.

The assessment gives a timeline and costs to help firms make decisions on what to tackle first and what it may want to consider in the longer term. It is the firm’s decision what to do next and how.

By using FinServ for this exercise, unlike other consultants, the job does not end at giving the firm recommendations. FinServ is available to help implement all the suggestions, provide assistance in choosing the right technologies, service providers, processes and procedures to ready the firm for present operations as well as for the future.

While the operational assessment does not look at whether and how a firm might go into another business, like loan servicing, the process does look at operations where targeted improvements will make jobs more efficient and scalable. Some growing firms worry that every time they add a new fund or strategy, they will need to hire more persons, adding to the costs and making it difficult to scale the business. For them, outsourcing options and third parties that can assist them and make more staff unnecessary may be better options than adding to the employee list.

Assessments are also made on third party providers, like fund administrators. By looking closely at what a fund administrator provides, they could request more services and gauge whether the amount of money the administrator is charging is close to the costs for similar businesses. The assessments are holistic, looking at all the processes of the entire firm.

Whether the need for an operational assessment is necessitated by operational due diligence by investors, a more complex investor base, firm growth or just a health check after a few years of operations, the process is geared to help tighten processes and procedures, streamline controls, and get the firm to the desired future state where it is capable of being more efficient and making more informed decisions. A fund’s infrastructure should never dictate what trading strategies are permissible or impede a business decision.

Even firms that believe they are relatively straight forward as they only do a small number of investments or trades may be challenged by the complexity of regulatory filings, the different types of data needed for a variety of purposes and a complex investor base.

Conclusion

FinServ Consulting, with years of experience working with a wide variety of asset managers, brings its knowledge and expertise to the operational assessment process – and does not leave the client with a list of “to-dos”. It helps in the implementation of the suggestions to create a firm fit for purpose now and in the future.

To learn more about FinServ Consulting’s services, please contact us at info@finservconsulting.com or (646) 603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

Robust Integration with Salesforce

Integrating external data feeds from your Administrator can facilitate operations and eliminate many of the daily bottlenecks faced by employees. Investor Relations teams may struggle to adequately communicate key performance and investment data to investors if they are simultaneously juggling numerous information sources. Directly feeding Administrator data into Salesforce will allow them to navigate a singular system while answering critical questions. Moreover, you can finally eliminate your countless excel files and the associated processes that mandate excessive manipulation.

Salesforce boasts impressive reporting and data visualization functionality that will enable your firm to draw deeper insights. The amalgamation of Salesforce Reports, Dashboards, and real time data will allow your organization to create visualizations highlighting key investor and performance metrics. Thus, augmenting personnel’s ability to anticipate client needs and answer their questions. FinServ has developed an assortment of pre-built reports and dashboards that isolate data pertaining to investment strategy, region, fee structure, performance, and more.

How to Integrate Your Data

Salesforce offers three primary tools for uploading data into Salesforce: Data Import Wizard, Data Loader, and dataloader.io. Each tool is applicable in its own right with differing use cases and functionality. The Data Import Wizard does not require installation and can easily be found by performing a quick search within Setup. Once you open the Data Import Wizard, it is as simple as selecting your CSV file and mapping the fields via the Salesforce Interface. Although the Data Import Wizard is a useful tool for basic uploads, it’s record count is limited to 50,000 and it cannot export data. The Data Import Wizard can be leveraged for both Custom Objects and Standard Objects such as Accounts, Contacts, Campaign Members, Leads, and Solutions.

Data Loader is a more robust data integration solution than Data Import Wizard. It is an external client application and therefore requires installation. The Data Loader facilitates the importation of 5,000 to 5 million records and is inclusive of both data exportation and deletion functionality. Users can specify configurations with the user interface or command-line interface. More advanced users can use the command-line interface to automate their data processing needs. However, the command-line interface is limited to Windows users and uses the Salesforce Object Query Language.

The final and most developed option is the cloud based MuleSoft solution known as dataloader.io. Similar to Data Loader, dataloader.io boasts importing, exporting, deleting, and scheduling capabilities. However, it can pull data from a variety of sources such as Box, Dropbox, FTP and SFTP repositories. Data Loader’s functionality is dependent on the package offering (Pricing Information) and has 3 editions that are priced at $0, $99, or $299 per month per user. The number of records, file size, and related objects ranges from 10,000, 10MB, and 1,000 to Unlimited, 100MB, and 100,000 per month.

How FinServ Can Help

FinServ’s completion of hundreds of projects spanning the Back, Middle and Front Offices for more than 40 of the top 100 Alternative Asset Mangers has enabled an expertise in industry processes, technological solutions, database management, and more. Additionally, FinServ has a deep understanding of the granular details associated with constructing a customized data model that fulfills your funds operational needs. FinServ is an accomplished integration partner due to countless experiences with Administrators and other Third-Party Data Sources.

Identifying the correct data may appear intuitive, but it is a common pain point throughout the industry. FinServ will host sessions with your various teams to identify and document their requirements. Thus, enabling the structured categorization of necessary and superfluous data. Directly integrating data into Salesforce allows for the elimination of unnecessary calculations that often mandate reconciliation. Subsequently reducing strain on your infrastructure and employees to allow for concentration on value rather than performing endless maintenance.

FinServ’s role extends well beyond the traditional tasks associated with integrating your data feeds. Business processes optimization and the identification of enhancements will originate from more than 15 years of experience within the Alternative Asset Management industry. FinServ will consolidate systems, document procedures, ensure successful implementations, and redesign processes to construct a simple and efficient approach that supports both your business and personnel.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

Shadow Accounting – Benefits, Issues, and Realities

Overview

Many investment funds outsource their back office and fund administration services to third-party administrators. Fund administration services typically include calculation of net asset value (NAV), daily, weekly or monthly P&L reporting, fee calculations and other activities that constitute being the official books and records. The reasons for using third-party administrators are well documented and typically include investors’ preference for an independent firm to oversee a fund’s financials. In addition, third-party administrators provide the ability to scale and often provide a sliding pricing model that goes up when a firm does well and down when a firm does not. Lastly, firms can take advantage of admin technology without the need for supporting this infrastructure in-house.

Shadow accounting is the process of maintaining an additional set of financial books for the purposes of comparison with the third-party administrator.

Reasons for shadowing your administrator

| Speed of reporting | Maintaining their own set of books affords funds the flexibility to determine their own schedule. While third-party administrators are held to service level agreements, they often do not cover ad-hoc reporting requirements and if they do, the agreements usually do not offer turn around times that are typically expected by senior management. Having your own systems and ability to report allows funds the opportunity for off-cycle reporting and if applicable, real-time analytics. |

| Reconciliation with the Fund Administrator | As mentioned previously, the responsibilities of an outsourced administrator can be broad. They’re often responsible for producing the NAV which has a direct correlation to the calculation of fees. Since there are many factors that go into these calculations, funds often like to have a separate process for producing these calculations to compare with their admin. When the numbers match, all is well. When the numbers are different, an investigative process will be conducted to determine the correct values. |

| Aggregation of multiple administrators | When funds have a multi-fund administrator model, it is sometimes difficult to get a complete picture across the fund family. Maintaining a shadow set of books allows funds to report across individual strategies and produce a holistic view of their performance. |

| Connection to risk and reporting systems | As part of the overall fund technology infrastructure, financial data is often sent downstream to allow for risk reporting, budgeting and forecasting, P&L data and other analytics. While this may not be the primary reason for shadow accounting, funds can become dependent on this data and having this data in-house may provide better data and allow for better reporting. |

| Lack of comfort/trust | Certain funds feel like they must outsource their back office and middle office operations since investors require it. When going through this process, if the admin fails to garner the trust of the in-house fund accountants, the fund may feel uneasy about eliminating their internal calculations and controls. In this era of increased regulatory scrutiny, it is more important than ever to have accurate information as incorrect filings can lead to fines and penalties. |

| Valuation accuracy | Producing a second set of books gives the fund an opportunity to apply their valuation and pricing strategy to their portfolio. In theory, this should match the admin’s valuation policy, but many times differences surface due to alternative market data sources. In the end, shadowing the portfolio leads to informed decisions when valuing investments. |

| Investors and allocators want it | There are investors or allocators that strongly prefer when a fund shadows their admin. It provides another level of control and has a positive impact on the due diligence reports conducted by potential investors. With the number of firms competing for investors, providing evidence of increased controls through shadow accounting has become a requirement. |

Full Shadow Accounting vs. ‘NAV lite’

NAV lite (or NAV light) is the process of taking in key inputs from the admin or other external sources and performing a check on the NAV calculation. In addition, it is common for the internal fund team to perform fee calculations as both an input and output to the NAV. Funds choose to do this to gain a level of comfort and provide senior management with confidence that the calculations are correct. The advantages of this approach are staffing requirements are reduced, and a full-service fund accounting system is not needed. Having confidence in the calculations is often enough to ensure the accuracy of the administrators. Some would argue however, there is no substitute for starting from the trade and entering all the debits and credits needed to calculate a NAV and a full set of financials in order to ensure accuracy. Shadowing only the NAV involves dependencies from the data being supplied by the admin and therefore comes with risks that mistakes could be made and the NAV can still be incorrect.

The Verdict

A recent survey indicated that over 80% of all investment managers perform some level of shadow accounting. It is rare for an investment firm to have the ability to raise capital without additional scrutiny that has become the norm in the industry. Investors and allocators have a large population of investment managers to choose from and have applied increased scrutiny as part of their due diligence. Most allocators have made it clear that shadow accounting is a requirement or at least desired. In addition, the data investors, auditors, and regulators are asking for is easier and quicker to produce when internal systems can be used. Therefore, funds have overwhelmingly made the choice to fully shadow or partially shadow their admins.

The Realities of Shadow Accounting

The realities of this decision are the increased investment from a cost and resource perspective, in a fund’s infrastructure. Funds are increasingly choosing order management systems and performance management applications that either has an accounting engine or can produce reports that can be used to produce a NAV. Choosing a system or systems to perform this function can be difficult and proper resources should be dedicated towards the selection and implementation. Similarly, choosing an outsourced shadow accounting provider is a critical decision that should be made after proper vetting. All funds are unique and therefore making decisions based on what worked for other funds typically leads to failed implementations. Choosing a system or vendor is a long term decision that is difficult to undo and requires attention to detail and diligence to get it done properly.

FinServ Consulting has been providing advisory, technology and business solutions to investment firms for over 15 years.

For more information on how we can help or guide your strategic direction, please contact us at info@finservconsulting.com or 646-603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

The Changing Fund Administration Landscape

Recent News

The fund administration business is no stranger to the merger mania that has affected other service providers in the financial services industry. In the race to build out the most complete, feature-driven platform, these outsource providers have taken the route of buy (versus build). Recent examples include State Street buying Charles River Development, JP Morgan moving part of their business to Arcesium’s technology platform and SS&C buying Eze Software. These are a few of the more well-known names in the industry, but there are much more. The common denominator in these three cases is that in an effort to build out and expand their product offering, these administrators have chosen to buy a complementary product rather than develop something in-house.

How Did We Get Here?

To understand today’s landscape, it’s worthwhile to go back in time just a few years to give some context. As recently as ten years ago, most fund administrators were perfectly happy to strike a NAV and run some basic reconciliations for a hedge fund (and were paid handsomely for it). As the industry went through a transformation, asset managers in search of alpha started to increase the breadth of their trading. With regulation added to the mix, not only did asset managers have to contend with internal and investor reporting, they had to now consider things like FATCA and Form PF. As a result, fund administrators were finding themselves having roles in the front, middle and back office.

A few of the common themes that we’ve come across in our research is that investors have started having an increased appetite for analytics. This is in turn requires their fund administrators to be able to sate their appetite. If the platform has no capability to handle big data or provide business intelligence, they will immediately find themselves at a disadvantage. One reason why JP Morgan moved part of their fund administration business to Arcesium was for its one-stop shop of integration across the technology stack. In this new paradigm, clients would have access to their own technology and an in-place data model, while providing Middle Office services, NAV calculation and investor reporting.

Joan Kehoe, global head of JP Morgan Alternative Investment Services said, ‘we have seen opportunities to streamline and automate this two-way information transfer between those records we keep as an administrator and our clients’ systems, a task that has historically been complex due to different applications, data models, sourcs of information, and timing.’ In this case, we can go back to the buy vs build question that everyone faces. In this case, even a well-capitalized corporation like JP Morgan decided that there was no internal appetite to build all of these integration points. Instead, they went out to the market and found a service provider in Arcesium, which has already built a tried and tested product. Arcesium today manages more than $100bn in AUA (assets under administration) and counts Balyasny, Blackstone Alternative Asset Management and DE Shaw as clients.

The eternal hunt for alpha has also forced fund administrators to adapt to their clients’ trading activities. Being able to handle multi-asset servicing in an automated fashion via the cloud has become a key driver to fund administration expansion. In the past, with relatively small volumes being traded by few clients, administrators could live with manual processes in the short term. In today’s world, increased volumes from multiple clients require automated solutions. When you add to the mix, algorithmic and high frequency clients, automation has become a must-have. When SS&C closed on the purchase of Eze Software in July 2018, industry veterans pointed to Eze’s new cloud platform, Eclipse, as a prime driver for the acquisition.

The world’s largest fund administrator, BNY Mellon, which has $33.1 trillion under custody and/or management, has recently started an initiative to revamp their Middle Office platform. Their decision included a combination of buy and build. They have a proprietary OMS and their derivatives system remains Summit, which is a product from Finastra. There are plans to upgrade their Collateral systems with new messaging software. Their fund accounting system remains Eagle, which they purchased almost twenty years ago.

It should be noted that asset managers have also looked to fund administrators to outsource their back office operations. Back in 2011, Bridgewater Associates made the decision to outsource their back office to BNY Mellon. This involved carving out roughly 200 employees and turning them into BNY Mellon employees, while still employing them out of the same office in Westport, CT.

Integration of the Front, Middle and Back Offices

Like any other industry, added competition causes everyone to become leaner and provide improved, scalable service. One way of doing this is finding and choosing the best-in-breed component for your product.

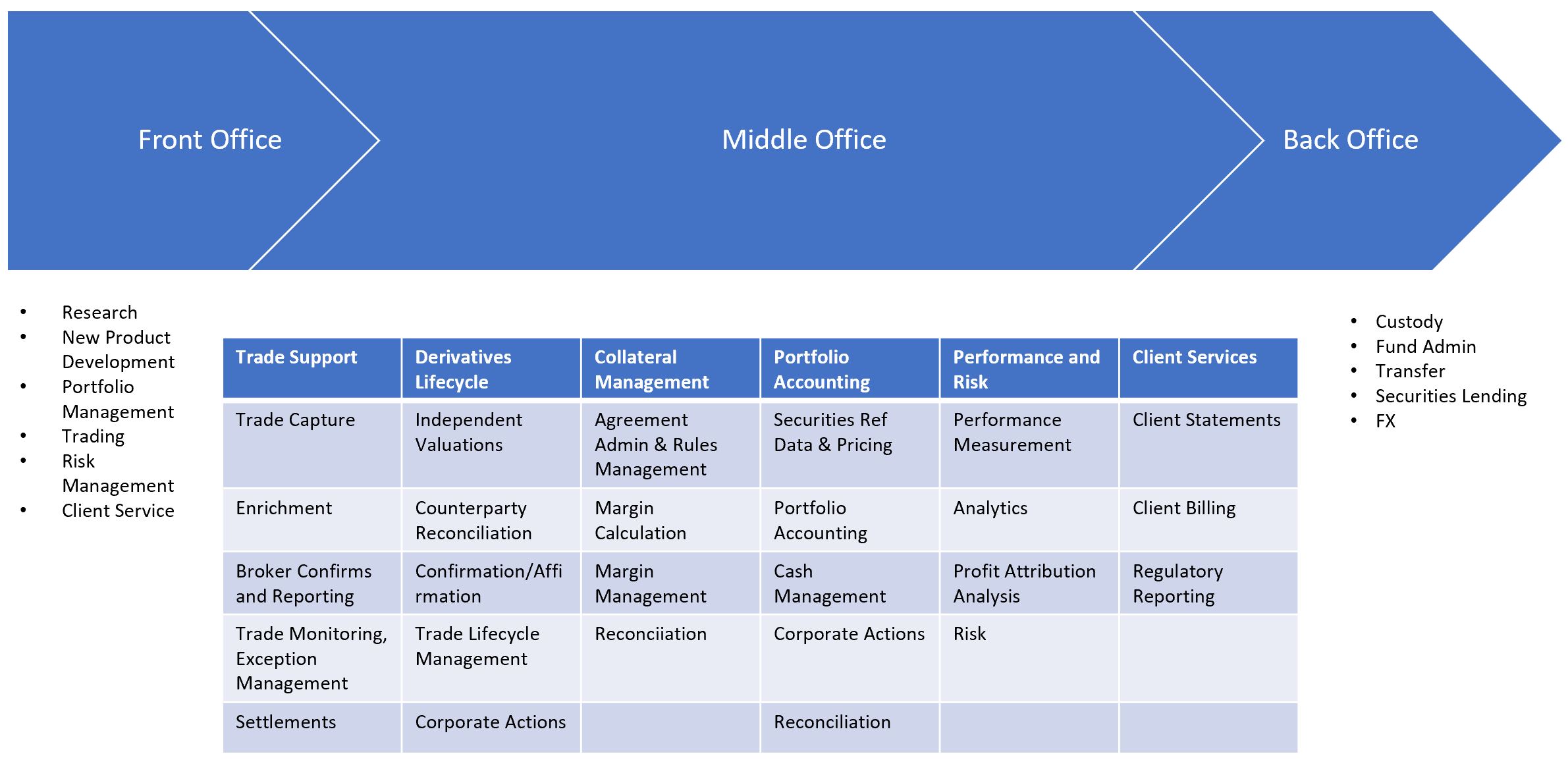

When you take a look at the chart of Front-to-Middle-to-Back Office activities, you can see that the Middle Office function has a lot of opportunities by which fund administrators can improve and scale their offering. This area has traditionally been the driver of the mergers we mentioned in the beginning. When State Street bought Charles River Development, it was for their award-winning trade capture/order management offering. They likely looked at competitors like Blackrock, who for years, have had their own OMS system in Aladdin. Lou Maiuri, the head of State Street Global Markets accurately summed it up when he said, ‘the reality is building things internally, starting this from scratch organically, it’s a long journey.” Acquiring another market-leading vendor also ensures that your existing client base is much more likely to continue buying your services.

But, this can be a double-edged sword. When there is opportunity for integration among all the different Middle Office functions, there is also ripe opportunity for things to go wrong. If you can imagine each vertical (ie Trade Support, Derivatives, Collateral, Accounting, Risk and Client Services) coming from a separate module or vendor, there could be up to 6 different disparate systems in the Middle Office! Imagine what could go wrong as a fund administrator attempts to ensure data flows automatically between the six systems. Some of the pain points we’ve seen is: 1. keeping a golden source of trade data as it goes through the trade lifecycle; 2. ensuring that Collateral is kept up-to-date in the Derivatives system and 3. ensuring reference data is persisted throughout the Middle Office.

As much as you can expect each vendor to have integration points upstream and downstream, fund administrators have realized the best way to mitigate data risk is to own your platform and the data that comes with it. Past market surveys that we’ve seen have noted that the three most important factors in selecting a fund administrator are: technology ease of use, technology ease of integration and willingness to customize. What better way to ensure your technology is easy to use and integrate than having control of the product and the platform, in-house?

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

Now Is the Time to Get an Affordable Trading Platform for your Fund

A new set of enterprise level trading systems has been added to the marketplace with much more reasonable price points. Funds that have been holding off on implementing an enterprise-level system to manage their Execution Management (“EMS”), Order Management (“OMS”), Portfolio Management (“PMS”), Fund Accounting and lite Risk requirements should consider re-examining the market for the best options. Despite the lower price point, these applications offer robust core functionality for funds with moderate trade volumes. These systems also offer true straight through processing (“STP”) for many types of equity focused funds. FinServ is seeing an increase in its client base of hedge funds looking towards more cost-effective Portfolio Management platforms.

The majority of these offerings are coming from new software firms in the marketplace. Historically, the biggest challenges of implementing software from startups, or relatively new firms has been a lack of maturity, or the inability to cover certain asset classes. Since many systems were built for one specific fund’s assets or business approach, it often proved far too challenging to take the software that worked well for that one fund and extend its functionality to cover the multiple asset classes and potentially higher volumes that a more complex or larger fund would have. While some of these challenges still exist, and you have to assess each new product independently, many of the latest offerings have passed FinServ’s intensive vendor selection reviews.

Our clients are finding that the cost savings are compelling enough to choose an up and coming software provider over the old stalwart trading platforms that come with a very high price point and here are some typical price point differences we are seeing:

The majority of FinServ’s clients that have a long/short strategy or are lower volume shops, are a good fit for these new solutions. The following topics highlight key areas that will indicate if your fund is a good fit for these systems:

Product Mix – Historically, derivative and hedging, or more exotic asset class support were missing in the newer software choices. Now, the asset class and derivative coverage exist from the majority of these vendors. It is important to note that, as these companies mature, there is some flexibility and patience required, as the asset types are expanded. However, for many of our clients, the cost savings are worth the investment and time required as new functionality is built out.

Trade Volumes – High trading volume shops are not a good fit for these systems because these newer systems cannot currently support the performance demands of the very high transaction flows. However, for funds with trade volumes between 10 and 200+ trades on a weekly basis, who do not trade exotic asset classes, these funds are a good fit for the newer systems in the marketplace.

What is Driving Funds to Require a Portfolio Management System

A number of our clients are anxious to move off Excel, as they see Excel-based systems as a major operational risk. The move is being driven by funds who don’t like to rely on their administrator for reporting that is critical and urgent to their day to day operations. Historically, funds with anything but a very simple mix of asset types did not have many options besides the high cost of systems like SS&C’s Geneva. Now, these funds can choose from a handful of well architected and efficient platforms that can support: Execution Management, Order Management, Portfolio Management, Fund Accounting, lightweight Risk Management & Compliance, as well as Reconciliation functions all under one application.

| Topic | Historical | Current |

| Desire for Real Time Reporting |

|

Even our smaller clients are moving to shadow accounting for multiple reasons:

|

| Meeting Regulatory Requirements |

|

Investor Demands

|

| Reducing Operational Risk |

|

Leveraging a portfolio accounting platform to reduce operational risk by interfacing directly with market data providers, brokers and counterparties

|

| Simplifying Operations & Technical Infrastructure |

|

The new software companies are offering a true straight through processing (“STP”) experience that allows a fund to go from the front to back office with one system. Support true Portfolio Management System capabilities including tagging at the trade and security level for P&L and exposure reporting Pre and Post trade compliance capabilities are now an out of the box feature of most of these systems Key Advantages of 1 system – Front to Back

|

In the following case study FinServ highlights one of our most recent clients who made the move to a new system:

| Case Study – How One Fund Added Shadow Accounting & Automated Reconciliations |

|

A Long / Short Equity shop with over $2B AUM was looking for a shadow accounting solution that would allow for daily reconciliations with its Third Party Administrator’s (“Admin’s”), Prime Broker’s (“PB’s”), and Counterparties and would provide day T+0 reporting to assist with portfolio exposure analysis and same day P/L analytics. The existing process included manual daily reconciliations consisting of logging on to websites, manually transcribing position, market value, and cash balances and comparing these records to the Admin, the street and internal records. This process was error prone, time-consuming and placed a huge reliance on their fund administrator. If new counterparties were added, it compounded the issue and placed an undue burden on the fund accounting and operations staff. The fund began looking for an in-house portfolio accounting solution that would not only allow for a full shadow, but could assist with the reconciliations and reporting requirements. The fund contracted FinServ to assist with the selection. The requirements called for a solution that could be hosted to reduce the burden on the limited internal IT support staff. The system also needed to be capable of supporting asset classes including CDS, CMBX, TRS and several Fixed Income products. In addition, the fund anticipates expanding its asset class to include Bank Debt and other Credit positions in the near future. The system also needed to be integrated with their existing OMS, downstream reporting software and potentially a future treasury, data warehouse and risk application. FinServ documented the existing infrastructure and created future state diagrams depicting the optimal end state. FinServ conducted multiple interviews with the fund operations and accounting staff to understand the key user requirements and current pain points. After a thorough selection, which included a detailed cost analysis, the fund and FinServ selected Enfusion’s Integrata Fund Accounting solution. FinServ and Enfusion took the lead to setup the fund’s structure, load opening balances and connect with the Order Management System (“OMS”). The fund’s admin, prime broker and several counterparties were interfaced directly in the system and reconciliation functionality was established to highlight differences with cash, market value and position data. Financing agreements were established for each unique Swap to automate the daily financing accrual. In addition, Bond interest, Dividend and other automated interest entries were established. An interface with Bloomberg Data License was put in place so prices could be snapped throughout the day. Positions and Cash balances were reconciled with the Fund Admin’s NAV packs. Trade data received from the OMS is reconciled daily. Reconciliation activities which used to take hours each day are now automated. Breaks are identified immediately and remediated. Reporting is now available the same day and includes daily calculations that were previously only accessible at month end. In addition, wash sales and other tax lot reporting is more accessible and allows for more informed trading decisions. Future phases will see Enfusion feeding the OMS with start of day positions and feeding downstream reporting applications which are currently fed by the administrator. Enfusion was the right choice for this fund which is enjoying greater flexibility, increased accuracy and quicker access to data.

|

How FinServ Can Help

An experienced integrator can make a huge difference in your implementation. Pointing out areas like where you can save significant costs with your software provider is just one key area where the right partner will make a massive difference to the success and ultimate cost of your implementation. A partner like FinServ will also make sure you consider all aspects of your business. It is important to not only consider existing needs but also understand where the firm may be headed in the future.

Our clients have found significant benefits in both cost savings and overall operational efficiencies through implementing many of the new Trading Platforms. Even smaller funds now require in-house systems and have a strong desire to eliminate external reporting dependencies. The greatest barrier against undertaking a project of this size and complexity is often the availability of key staff. FinServ has the capability to provide investment fund best practices, subject matter expertise, and a hands-on approach, to ensure your project can be implemented successfully without jeopardizing the daily and monthly responsibilities of key staff.

Strong project management and a tried and true systems integration methodology are also critical to a successful systems implementation. In the past 12 years, FinServ Consulting has saved our client’s millions of dollars by delivering each project we perform, on time and on budget. While the new software companies have strong technologists and architects, they still lack a focus and expertise in core project management and often get distracted trying to manage too many clients at one time. Our clients usually run very lean and having a member of their firm shift all their responsibility to a full-time project is not feasible. By having a consultant who is dedicated to the project and stays on top of all open items including managing the software vendor, we find that projects are completed in a fraction of the time of other implementations where no dedicated consultant is utilized.

Our team can help you determine if you are a good fit for one of these systems and help to estimate the costs and time for your implementation. For more information, please feel free to contact us at info@finservconsulting.com or (646) 603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

6.5 Proven Tips for Selecting the Right Third Party Administrator

The market landscape for Third Party Administrators (TPA’s) is changing rapidly and many Hedge Funds and Private Equity firms are struggling to make sense of these changes. The major players in the marketplace are consolidating, but new Fund Administration options are appearing almost everyday. The current state of the market makes selecting the right TPA for your fund more difficult than ever.

Funds are wise to utilize a structured approach when evaluating the market for TPAs. A structured approach helps ensure that you select the best service provider to fit your firm’s unique strategy, product mix and approach to operations. Utilizing a consultant can help make certain that your Administrator selection project occurs on time and within budget.

FinServ Consulting’s Third Party Administrator selection services have already helped numerous leading Alternative Asset Managers select the right Third Party Administrator to support their growth. FinServ’s team has spent more than 200 hours analyzing the marketplace in over 20 different performance categories around functional, technical and regulatory requirements. FinServ’s experience working with Funds and TPAs has led to an industry leading perspective on the TPA Market. FinServ understands the complexities of the marketplace and can help provide guidance on how to select the best TPA for your firm. FinServ’s team places emphasis on the following best practices for considering a new Fund Administrator.

(1) Understand your Firm’s Unique Complexity

The first step in selecting the right Administrator is to understand what makes your firm unique. The right Administrator will be able to understand and even help resolve this complexity. Does your firm have both Private Equity and Hedge Fund structures? Do your investors have certain reporting requirements? Does your IT team have extremely rigid security concerns? It is imperative to ensure that the TPA your firm selects is well equipped to handle your unique operational challenges. It is also important to consider the future strategic direction of your fund. Some Administrators cannot service certain fund structures like 40ACT or UCITS funds, and will be unable to support future growth in these areas. Understanding your firm’s current objectives and future direction is crucial to selecting the right administrator.

(2) Define Key TPA Capabilities in Working Sessions

Holistically understanding your firm’s operations is also an important step in selecting the right administrator. Different functions within a fund have unique perspectives on what is important; so it is crucial to involve all stakeholder groups in the process. Furthermore, clients who operate in different geographic regions can have unique requirements that should be incorporated (i.e. specific regulatory requirements or an understanding of the local culture and methods of operation). FinServ’s methodology includes conducting workshops with different operational areas in the firm to drive the requirements that form the basis of the Request for Proposal (RFP). Creating working groups allows you to ensure that all requirements are captured, and every department feels they are part of the selection process. This inclusion drives ownership and buy in for the vendor that is ultimately selected.

(3) Spend Time on the Request For Proposal

The RFP is an extremely important document that breaks down a fund’s requirements into key areas for the vendors to focus on. The RFP will organize your firm’s key processes into well-defined technical and functional requirements. A quality RFP presents your fund’s information in a manner that will elicit meaningful vendor responses to address your key challenges. The information requested from the Administrators in the RFP will include details on the Administrator’s organization, client base, capabilities, service levels, pricing, conversion methodology, and operating model. The RFP should be a comprehensive document that serves as a basis of comparison for all of the vendors. Vendor responses should be evaluated both qualitatively and quantitatively to narrow the already short vendor list to 2-3 finalists that can be further drilled down upon.

(4) Create Quantitative Scoring on the RFP

Often selecting a vendor can become a very emotional decision. You may like the salesperson or the team, but buying based on emotions can often lead to the wrong choice. In order to separate the emotional aspect of the sales process, funds are wise to leverage a quantitative approach to balance their qualitative assessment. Utilizing quantitative scoring on the RFP allows you to compare vendors across the various dimensions that are important to your organization. The different requirements from the RFP should be prioritized and ranked, and each vendor’s response should be evaluated. Hard metrics (i.e. processing times) are preferable, but where hard metrics do not exist, vendors should be rated on a 1-5 scale indicating their strengths and weaknesses in the area.

Quantitative scoring allows your firm to make an informed decision by objectively evaluating each TPA to provide the best overall picture of which Administrator is right for your firm.

(5) Scripted Vendor Demos

The best way to ensure that a vendor can provide the services they promise is to have them demonstrate their capabilities. Sales demonstrations often focus on specific features that the sales team wants to highlight, almost exclusively focusing on their company’s natural strengths. The FinServ Consulting scripted demos focus exclusively on the functionality important to your firm. FinServ works with funds to identify their most complex operational challenges and break them down to a series of instructions to be performed by potential Administrators. FinServ has found that creating scripted demonstrations on all key requirements is a powerful tool for confirming vendor competence. Scripted demonstrations should outline exactly what you expect to see during the demonstration, and what the criteria for evaluation is. Ideally, the scripts should outline real-world scenarios using your company’s own data. This will allow you to see how each Admin handles specific requirements and allow for a meaningful comparison between the different vendors. It is also prudent to have your operational teams conduct Q&A sessions directly with the various vendors to help each key stakeholder group ensure their specific requirements are met, while building their understanding and comfort level with the process.

(6) Conducting Thorough Reference Checks

Conducting thorough reference checks is one of the most important steps in selecting an Administrator, but it is often the most overlooked. Many firms approach references as a check-the-box exercise, but funds are wise to conduct through reference checks using detailed questions. References are the best way to gauge if the Administrator will be able to perform with regard to the specific circumstances and challenges of your organization. Any administrator you consider should be able to deliver references of clients with a similar AUM and investment strategy. Your firm should ask the provided reference about the Admin’s ability to perform specific requirements as laid out in the RFP. It is also important to ask about their implementation experience, specifically, what their biggest frustrations were during the onboarding process. Asking detailed questions of the references not only uncovers key issues or areas to address with the TPA but will also reveal personal experiences that will help you get the most out of the selected TPA. FinServ has experience conducting thorough reference checks and can help guide your firm through this critical step.

(6.5) The Importance of the Team

The competency of the team supporting your account is absolutely critical, so having the ability to choose your team or have a say in who will be servicing your fund is key. The vendor’s approach to transitioning from their sales team to their onboarding and servicing team should be clear and strong. In our experience, weaker TPAs spend all their time selling and don’t clearly communicate to the onboarding or delivery team what was learned or even promised in the sales process. This means key items are missed in the onboarding process, which ultimately leads to very painful work to address the lack of communication with the TPA. You should specifically ask to involve the vendor’s core service team early in the sales discovery process. You should ask the support team questions related to your specific business challenges and evaluate their responses. Additionally, Admins service funds from different locations, so it is important to get a feel for how your account will be serviced, and who will be responsible for the different tasks. Selecting the right Third Party Administrator is an extremely important decision for Alternative Asset Managers. The market is filled with many options, and it is important to pick the right vendor. Selecting the wrong vendor can easily cost 2-3 times the amount of hiring a consultant to help you select the right TPA. Every fund is different, so it is important to ensure that any Administrator selected supports your unique operational approach. FinServ has worked with all of the top Administrators and has insight into each TPAs’ Front, Middle and Back-Office functionality, as well as their Investor Relations, Financial Reporting, Tax and other ancillary capabilities. FinServ utilizes an industry leading approach that is tailored to your organization’s unique needs. Our team has the expertise necessary to help your firm make sense of the TPA market and select the right vendor to best support your firm’s ambitions.

To learn more about FinServ’s TPA vendor selection methodologies and related services, please contact us at info@finservconsulting.com or (646) 603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

5 Best Practices for Onboarding a New Third Party Administrator

Onboarding a Third Party Administrator (“TPA”) is one of the most important projects that a Hedge Fund or Private Equity firm can undertake. Whether you are a new fund or you are switching to a new Administrator, your TPA will be a long-term partner and the strength of this relationship often begins with the onboarding process.

Onboarding a Third Party Administrator (“TPA”) is one of the most important projects that a Hedge Fund or Private Equity firm can undertake. Whether you are a new fund or you are switching to a new Administrator, your TPA will be a long-term partner and the strength of this relationship often begins with the onboarding process. Issues with an Administrator can undermine your entire operation, as TPA’s are vital components of accounting, operations and investor relations processes. FinServ Consulting has onboarded many TPA’s for our clients, and our experience has uncovered the following best practices for Hedge Funds and Private Equity Firms to consider when onboarding a new Administrator.

(1) Rely on the RFP

The first step in any TPA onboarding process is to conduct a formal vendor selection based on a detailed Request for Proposal (RFP). The RFP is a very important document in the onboarding process, and a successful onboarding often follows a strong vendor selection process. The most robust RFPs break down a fund’s requirements into key areas and asks the Administrator to demonstrate how they will address these requirements. The RFP is a record of everything that the Administrator has promised and is a great reference for all parties during the onboarding. Many firms hire consultants to create the RFP and conduct the Vendor Selection, as consultants can offer the perspective necessary to gauge the accuracy of responses and add valuable insight to the process. A well-structured procurement process offers numerous benefits as it helps establish expectations, leads to objective decision-making and frequently results in a lower price.

(2) Dedicate Project Resources

Strong project management is a vital aspect of onboarding any Third Party Administrator. Project Plans, Status Reports and Issue Tracking are often the difference between a successful onboarding and an unsuccessful one. Dedicated project resources, whether they are internal or external, can help with project management, reconciliations, data gathering and any issues that arise during the onboarding. Often, the Administrator will provide their own integration resources; however, these resources are often reluctant to push internal resources, as they are eager to maintain the relationship. This reluctance can lead to increased conversion times and additional costs. Funds are wise to dedicate internal resources to the onboarding, and FinServ’s experienced team is always available to help.

(3) Spend Time Negotiating the Service Level Agreement (SLA)

SLA’s lay out the framework in which the fund and the TPA operate. The on-boarding process should be viewed as a way to improve your firm’s key processes. The SLA is a great resource to document your internal processes and work with your TPA to improve them accordingly. Spend time negotiating the SLA and don’t be afraid to ask detailed questions such as where the work is being done,

who will respond to questions after hours and the number of points of contact. In addition, ensure that you review and agree on the formatting of all deliverables in advance. Working with your Administrator to improve the SLA can help your firm achieve higher levels of operational and cost efficiencies.

(4) Find a Great Team and Foster Collaboration

The strength of the Administrator relationship often comes down to the quality of the team working with your firm. Funds should demand to interview and approve the team prior to signing a contract. The names of the resources should be listed in the contract, and this team should preferably assist with the onboarding. Having permanent resources on your team from the start prevents issues with knowledge transfer and ensures everyone is on the same page. In addition, creating a strong working relationship with your TPA is also of vital importance, and face-to-face contact is the best way to accomplish this. Organizing social events (or asking the Administrator to) and holding monthly on-site meetings, will go a long way to fostering collaboration and co-operation between teams. In person meetings during the onboarding is also highly recommended. When communication is limited to phone and email, the possibility of misunderstandings is much higher.

(5) Don’t Make Assumptions

Administrators are often good at the complicated items but can struggle in areas that seem intuitive. Do not make assumptions about how the Administrator will handle something, even if it seems simple. This is especially true in a conversion. Just because your prior Administrator did something in a certain way; do not assume that the new Administrator will be able to replicate this. It is a best practice to assess all processes and get detailed demonstrations in advance. Items that need to be tweaked should be done so prior to signing on the dotted line. Funds all have unique processes and it is prudent to ensure that your Administrator will be able to handle even the smallest nuance.

FinServ’s Value When Onboarding a Third Party Administrator

FinServ Consulting is an industry leader in TPA Vendor Selections and onboarding and has advised numerous top Hedge Fund and Private Equity firms in selecting the right TPA. We have worked with all of the top tier Administrators and have insight into each TPAs’ Front, Middle and Back-Office functionality, as well as Investor Relations, Financial Reporting, Tax and other capabilities. Our team has the expertise to help your firm navigate the complicated TPA landscape.

To learn more about FinServ Consulting’s Third Party Administrator related services, please contact us at info@finservconsulting.com or (646) 603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.

Major Marketplace Changes Abound

The past few weeks have certainly provided some major changes in our alternative asset management marketplace. First the news that Citigroup was leaving the Fund Administration business took many by surprise and is leaving those who are administered by Citi wondering who will be taking over their fund administration. Just when that news was being absorbed, the even more industry impactful story of SS&C acquiring Advent Software sent shockwaves throughout the Administrator and Hedge Fund industry.

While Citi Fund Services was certainly a major player, there are many reasonable alternatives for funds that do not want to risk the wait and see how Citi decides to sell or spin off that business. While selecting the right Third Party Admin (“TPA”) is one of the most important decisions a fund can make I will not focus this blog entry on that topic. Visit our website for more insights at www.finservconsulting.com.

Advent Geneva is probably the single largest software name in the alternative asset management industry. While Geneva owns the less than sexy back office portfolio accounting space, all CFO’s and COO’s know how core this application is to their businesses. SS&C has certainly had a mixed track record in terms of the quality of their software so there is certainly reason for Hedge Funds to be wary of this move.

Most of the marketplace would probably be safe to assume that SS&C will not mess with Pete Hess and his team’s strong success so most funds are probably not panicking at this point.

The Third Party Admin space however should have several firms who have likely gone into full panic mode based on this news. At least one-third to one-half of the largest TPA’s are Advent Geneva customers and SS&C GlobeOp the Admin arm of SS&C now stands to gain a major competitive advantage for those TPA’s who will remain on Geneva. Only time will tell how that side of the transaction plays out but it is safe to say that SS&C GlobeOp will look to use this as a key selling point to gain market share.

For the TPA’s who do not use Geneva they now are looking at a much stronger competitor than they had just a week ago and they should expect that their clients who use Geneva will likely at least take a look at SS&C at some point if their services do not meet expectations in the near future.

More to come on this major change in our industry…

For more information about our services related to third-party administrators and SS&C, please feel free to contact us at info@finservconsulting.com or (646) 603-3799.

About FinServ Consulting

FinServ Consulting is an independent experienced provider of business consulting, systems development, and integration services to alternative asset managers, global banks and their service providers. Founded in 2005, FinServ delivers customized world-class business and IT consulting services for the front, middle and back office, providing managers with optimal and first-class operating environments to support all investment styles and future asset growth. The FinServ team brings a wealth of experience from working with the largest and most complex asset management firms and global banks in the world.